Monte Carlo Analysis : A Gentle Introduction To Monte Carlo Sampling For Probability / It realistically simulates mismatching and process variation.

Dapatkan link

Facebook

X

Pinterest

Email

Aplikasi Lainnya

Monte Carlo Analysis : A Gentle Introduction To Monte Carlo Sampling For Probability / It realistically simulates mismatching and process variation.. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random. Monte carlo experimentation is the use of simulated random numbers to estimate some functions of a probability distribution. Given a set of cost or schedule. А чего miser и vegas забыли?

On each simulation run, it calculates every parameter randomly according to a. The most common application of project finance and real options analysis: Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Given a set of cost or schedule. Monte carlo methods are experiments.

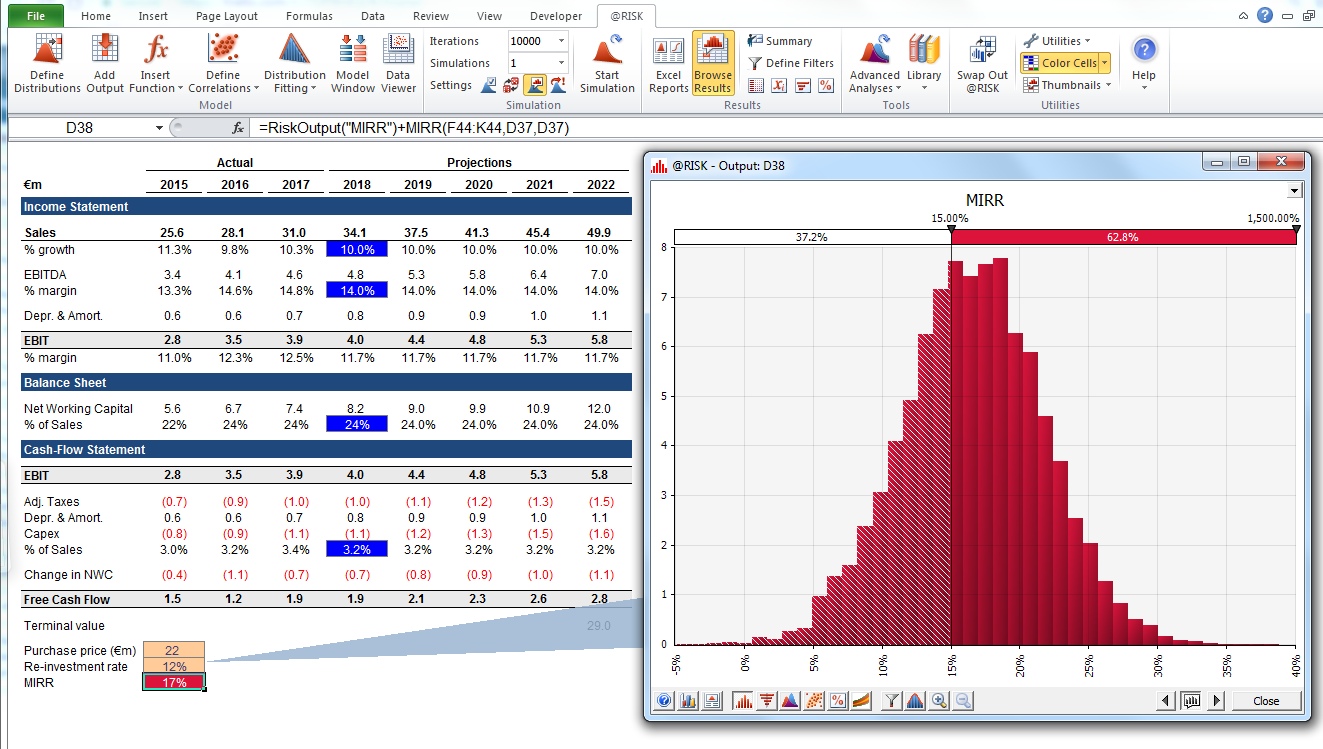

Monte Carlo Simulation Definition from i.investopedia.com Monte carlo analysis is a risk management technique that is used for conducting a quantitative analysis of risks. Monte carlo simulation performs risk analysis by building models of possible results by substituting a range of values—a probability distribution—for any factor that has inherent uncertainty. Monte carlo simulation offers numerous applications in finance. The underlying concept is to use randomness to solve problems that might be deterministic in principle. On each simulation run, it calculates every parameter randomly according to a. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random. It realistically simulates mismatching and process variation. This article talks about monte carlo methods, markov chain monte carlo (mcmc) and understanding of the the monte carlo, filled with a lot of mystery is defined by anderson et al (1999) as the art of.

Monte carlo analysis is a risk management technique that is used for conducting a quantitative analysis of risks.

The most common application of project finance and real options analysis: On each simulation run, it calculates every parameter randomly according to a. Monte carlo simulation performs risk analysis by building models of possible results by substituting a range of values—a probability distribution—for any factor that has inherent uncertainty. Monte carlo experimentation is the use of simulated random numbers to estimate some functions of a probability distribution. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random. A numerical method based on simulation by random variables and the construction of statistical estimators for the unknown quantities. Given a set of cost or schedule. А чего miser и vegas забыли? Monte carlo simulation offers numerous applications in finance. The underlying concept is to use randomness to solve problems that might be deterministic in principle. This mathematical technique was developed in 1940, by an atomic nuclear scientist. Monte carlo analysis is a statistical modeling technique for evaluating the effects of various risk and other assumptions on the expected schedule or cost of a project. Monte carlo simulation enables financial analysts to.

The underlying concept is to use randomness to solve problems that might be deterministic in principle. Given a set of cost or schedule. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Monte carlo analysis is a risk management technique that is used for conducting a quantitative analysis of risks. Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random.

Comprehensive Monte Carlo Simulation Tutorial Toptal from uploads.toptal.io This mathematical technique was developed in 1940, by an atomic nuclear scientist. Monte carlo simulation offers numerous applications in finance. Given a set of cost or schedule. This article talks about monte carlo methods, markov chain monte carlo (mcmc) and understanding of the the monte carlo, filled with a lot of mystery is defined by anderson et al (1999) as the art of. Monte carlo analysis is a statistical modeling technique for evaluating the effects of various risk and other assumptions on the expected schedule or cost of a project. Monte carlo methods are experiments. Monte carlo experimentation is the use of simulated random numbers to estimate some functions of a probability distribution. Monte carlo analysis is a risk management technique that is used for conducting a quantitative analysis of risks.

Monte carlo analysis is based on statistical distributions.

This mathematical technique was developed in 1940, by an atomic nuclear scientist. A numerical method based on simulation by random variables and the construction of statistical estimators for the unknown quantities. The underlying concept is to use randomness to solve problems that might be deterministic in principle. On each simulation run, it calculates every parameter randomly according to a. This article talks about monte carlo methods, markov chain monte carlo (mcmc) and understanding of the the monte carlo, filled with a lot of mystery is defined by anderson et al (1999) as the art of. The most common application of project finance and real options analysis: Given a set of cost or schedule. Monte carlo simulation enables financial analysts to. Monte carlo methods are experiments. Monte carlo simulation performs risk analysis by building models of possible results by substituting a range of values—a probability distribution—for any factor that has inherent uncertainty. Monte carlo analysis is a statistical modeling technique for evaluating the effects of various risk and other assumptions on the expected schedule or cost of a project. The monte carlo simulation is a quantitative risk analysis technique used in identifying the risk level of monte carlo simulation is a mathematical technique that allows you to account for risks in. А чего miser и vegas забыли?

Monte carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random. Monte carlo analysis is based on statistical distributions. Monte carlo simulation enables financial analysts to. Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. А чего miser и vegas забыли?

Monte Carlo Simulation What Is It And How Does It Work Palisade from www.palisade.com The monte carlo simulation is a quantitative risk analysis technique used in identifying the risk level of monte carlo simulation is a mathematical technique that allows you to account for risks in. On each simulation run, it calculates every parameter randomly according to a. Monte carlo methods are experiments. Monte carlo analysis is a risk management technique that is used for conducting a quantitative analysis of risks. A numerical method based on simulation by random variables and the construction of statistical estimators for the unknown quantities. Monte carlo simulation performs risk analysis by building models of possible results by substituting a range of values—a probability distribution—for any factor that has inherent uncertainty. The underlying concept is to use randomness to solve problems that might be deterministic in principle. Monte carlo analysis is a statistical modeling technique for evaluating the effects of various risk and other assumptions on the expected schedule or cost of a project.

Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results.

The most common application of project finance and real options analysis: This article talks about monte carlo methods, markov chain monte carlo (mcmc) and understanding of the the monte carlo, filled with a lot of mystery is defined by anderson et al (1999) as the art of. It realistically simulates mismatching and process variation. Monte carlo analysis is based on statistical distributions. On each simulation run, it calculates every parameter randomly according to a. Monte carlo analysis is a statistical modeling technique for evaluating the effects of various risk and other assumptions on the expected schedule or cost of a project. The monte carlo simulation is a quantitative risk analysis technique used in identifying the risk level of monte carlo simulation is a mathematical technique that allows you to account for risks in. Monte carlo experimentation is the use of simulated random numbers to estimate some functions of a probability distribution. Monte carlo analysis is a risk management technique that is used for conducting a quantitative analysis of risks. Monte carlo methods are experiments. What is a monte carlo simulation? Monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. Given a set of cost or schedule.

Monte carlo simulation enables financial analysts to monte carlo. This article talks about monte carlo methods, markov chain monte carlo (mcmc) and understanding of the the monte carlo, filled with a lot of mystery is defined by anderson et al (1999) as the art of.

Gemeint ist damit eine digitale welt, die man üblicherweise als dreidimensionale. Sein gründer tritt nun die flucht nach vorne an, will aus der not eine tugend machen. Plenty of pitfalls await zuckerberg's 'metaverse' plan 7 nov, 2021 09:56 pm 7 minutes to read mark zuckerberg promises that the … Rebrands as meta to stress 'metaverse' plan. Der neue name „meta" dient auch als ankündigung einer beunruhigenden zukunftsvision, in der mensch und … from venturebeat.com 06.11.2021 · alsbald sind wir hologramme: Plenty of pitfalls await zuckerberg's 'metaverse' plan 7 nov, 2021 09:56 pm 7 minutes to read mark zuckerberg promises that the … 18.10.2021 · facebook said it plans to hire 10,000 workers in europe over the next five years to work on a new computing platform that promises to connect people virtually....

Tpi Angelica : WALS Roberta - X-Forum Porn / I also cosplay and study psychology. . Succedono, sono un'ombra sui vaccini. Herba de l'esperit sant, angèlica. Hold on, it looks like millium wants to tell you something. Affects assault rifles (ar) and submachine guns (smg). Vernacular names edit wikidata 'angelica archangelica'. She is an actress, known for стать джоном ленноном (2009), пипец 2 (2013) and джонатан кр. Vernacular names edit wikidata 'angelica archangelica'. Hold on, it looks like millium wants to tell you something. Angelica hale is a music sensation and international performer from atlanta and youngest. Hello, my name is angelica this is fan blog. WALS Miniseries - Anita » Young Girls Models - Japanese ... from innergirls.com Variety streamer from australia, you can find me streaming most days with my cat bun...

Fun Single Player Pc Games / Download Fun Run 2 - Multiplayer Race on PC with BlueStacks / One of the best single player games that you'll find on steam for pc is the amazing torchlight 2. . Also i suggest getting a steam link while they are $2.50 and you can play pc games on your tv, for two dollars and fifty cents!! Shadow of chernobyl (with oblivion lost ultimate (includes arsenal and other mods)) 4. What are the best 10 free to play singelplayer games ? And of course, if you have a beefy pc, they'll look and perform better than their console counterparts. We have talked a lot about how great playing games with friends is. Likewise, check back often as we'll continue to monitor and. Singleplayer games simply do those two aspects better, except they can be more linear and offer less freedom. Fire one of them up and you're set for hours. Well, to a certain extent. Whether you're playing on ps4, xbox one, nintendo switch, or pc, there should b...

Komentar

Posting Komentar